Personal Computing Procurement Intelligence

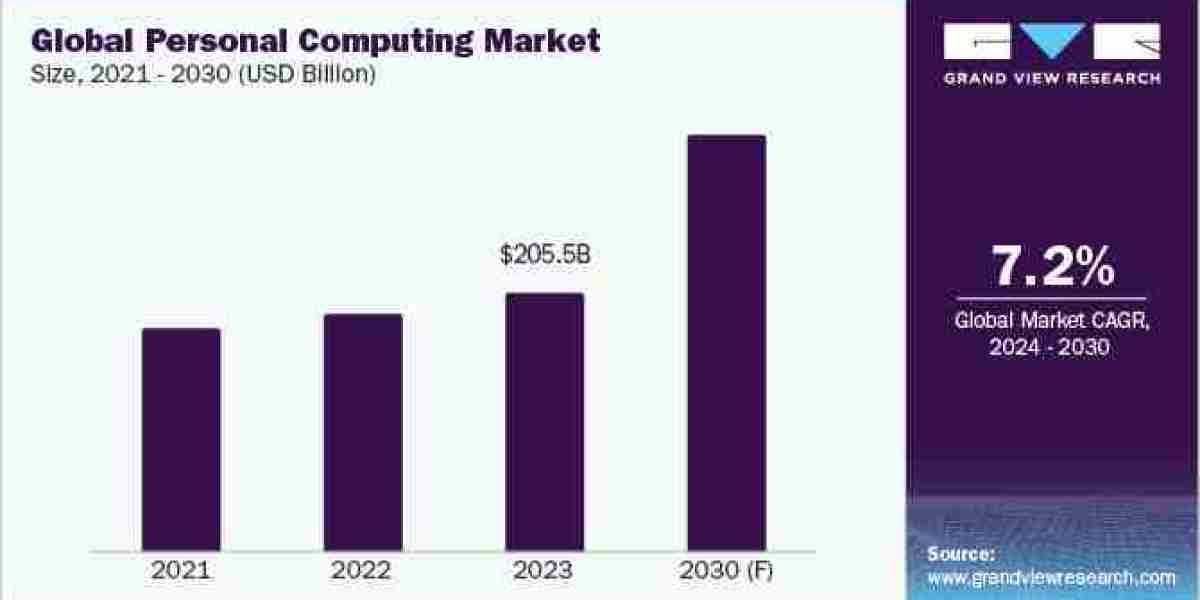

Procurement of personal computing services refers to the process of acquiring computers, related hardware, and software for individual use or within an organization. The global market size was estimated at USD 205.5 billion in 2023. Efficient procurement ensures optimal performance, cost-effectiveness, and compatibility with existing systems while maintaining a focus on security and user satisfaction. In 2023, North America held the largest share of the global market with 30%. This growth can be attributed to the dominating presence of key players, deployment of high-speed data infrastructure, advancements in laptop design and performance, innovation and sustainability initiatives by key players, and an increase in sales via e-commerce platforms.

Asia Pacific is poised to witness the fastest growth rate during the forecast period due to the rise of commercial establishments, rapid infrastructure development, surge in product usage by emerging economies, capacity expansions by key suppliers, improvements in technology, and an increase in government initiatives. Key countries driving the growth in Asia Pacific include China, India, Vietnam, Malaysia, and Taiwan, owing to efficient and low-cost production facilities, cheap costs of labor, and components such as semiconductors, and high demand growth from various commercial units.

These products are deployed by a wide range of end-users to execute a wide spectrum of day-to-day tasks, enable efficient administration, enhance employee productivity, and improve time management. Key end-users include corporate offices, educational establishments, government agencies, finance and accounting companies, and other sectors such as healthcare, hospitality, and retail. For instance, finance and accounting firms utilize these products for financial analysis, budgeting, and tax preparation. Government agencies use these products for managing public records.

Order your copy of the Personal Computing category procurement intelligence report 2024-2030, published by Grand View Research, to get more details regarding day one, quick wins, portfolio analysis, key negotiation strategies of key suppliers, and low-cost/best-cost sourcing analysis

Key technology trends impacting the growth of this industry include thin clients, Organic Light-Emitting Diode (OLED) panels, convertible 2-in-1 Designs, AR and VR integration, and slim and lightweight design. Convertible 2-in-1 designs enable products to seamlessly transform between two modes such as laptop and tablet. These designs have hinges that facilitate a 360-degree rotation, enabling users to switch effortlessly. In laptop mode, these products have a physical keyboard and trackpad for efficient typing and multitasking. When detached from the keyboard, they are converted into lightweight tablets, suited for on-the-go use. These convertible products are also equipped with touchscreens, making them ideal for note-taking, drawing, and navigating applications.

Key suppliers that provide personal computing items compete based on product pricing, customization, compliance with environmental standards, lead time optimization, innovation in design aspects, and improvement of security options. Buyers in this market have diverse options for budget range, product specifications, supplementary services, product warranty, and after-sales options. Regulatory directives in several countries require suppliers to comply with stringent standards related to product durability, quality standards, safety measures, waste recycling, and environmental impact.

The prices of these products are impacted by numerous variables. Key elements affecting the prices include variations in the prices of raw materials and components, supply chain and logistical issues, labor cost fluctuations, and licensing and compliance needs. Commonly used raw materials such as plastic, glass, metals, aluminum, arsenic, and silicon undergo significant variations based on feedstock and energy costs. On a similar note, costs of components such as semiconductors, batteries, and motherboards may fluctuate due to several reasons.

Personal Computing Sourcing Intelligence Highlights

- The personal computing market comprises a fragmented landscape, with suppliers engaged in intense competition.

- Due to the vigorous market competition, buyers within the industry have significant bargaining power and have the flexibility to switch to better alternatives.

- China and the U.S. are favored as low-cost or best-cost countries within their respective regions for sourcing personal computing products due to their reasonable costs of low costs of electronic components and the presence of well-established manufacturing units.

- The key cost components include raw materials and electronic components, labor, equipment, packaging and labeling, logistics and supply chain, and other costs. Other costs include R&D, rent and utilities, licensing and compliance, sales and marketing, general and administrative, and taxes.

List of Key Suppliers

- Acer Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Dell Inc.

- HP Development Company, L.P.

- Huawei Technologies Co., Ltd.

- Lenovo Group Ltd.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Sony Group Corporation

Browse through Grand View Research’s collection of procurement intelligence studies:

- Disposable Medical Gloves Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

- Loyalty Programs Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

- Helium Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

Personal Computing Procurement Intelligence Report Scope

- Personal Computing Category Growth Rate : CAGR of 7.2% from 2024 to 2030

- Pricing Growth Outlook : 5% - 10% increase (Annually)

- Pricing Models : Cost-plus pricing, competition-based pricing, bundled pricing, demand-based pricing, penetration pricing

- Supplier Selection Scope : Cost and pricing, past engagements, productivity, geographical presence

- Supplier Selection Criteria : Geographical service provision, industries served, years in service, employee strength, revenue generated, key clientele, regulatory certifications, product range, processor type, storage type, use of sustainable materials, delivery mode, customer service, and others

- Report Coverage : Revenue forecast, supplier ranking, supplier positioning matrix, emerging technology, pricing models, cost structure, competitive landscape, growth factors, trends, engagement, and operating model

Brief about Pipeline by Grand View Research:

A smart and effective supply chain is essential for growth in any organization. Pipeline division at Grand View Research provides detailed insights on every aspect of supply chain, which helps in efficient procurement decisions.

Our services include (not limited to):

- Market Intelligence involving – market size and forecast, growth factors, and driving trends

- Price and Cost Intelligence – pricing models adopted for the category, total cost of ownerships

- Supplier Intelligence – rich insight on supplier landscape, and identifies suppliers who are dominating, emerging, lounging, and specializing

- Sourcing / Procurement Intelligence – best practices followed in the industry, identifying standard KPIs and SLAs, peer analysis, negotiation strategies to be utilized with the suppliers, and best suited countries for sourcing to minimize supply chain disruptions